The Securities and Exchange Board of India (SEBI) has extended the timeline for the dispatch of the Consolidated Account Statement (CAS) by a few days. According to SEBI, this move is aimed at easing the burden of compliance. The decision was made after consultations with Asset Management Companies (AMCs), Depositories, and Mutual Fund Registrars and Transfer Agents (MF-RTAs). However, this extension leaves mutual fund investors at a disadvantage. Let’s explore the CAS system, its implications, and the potential repercussions of the delayed dispatch timeline.

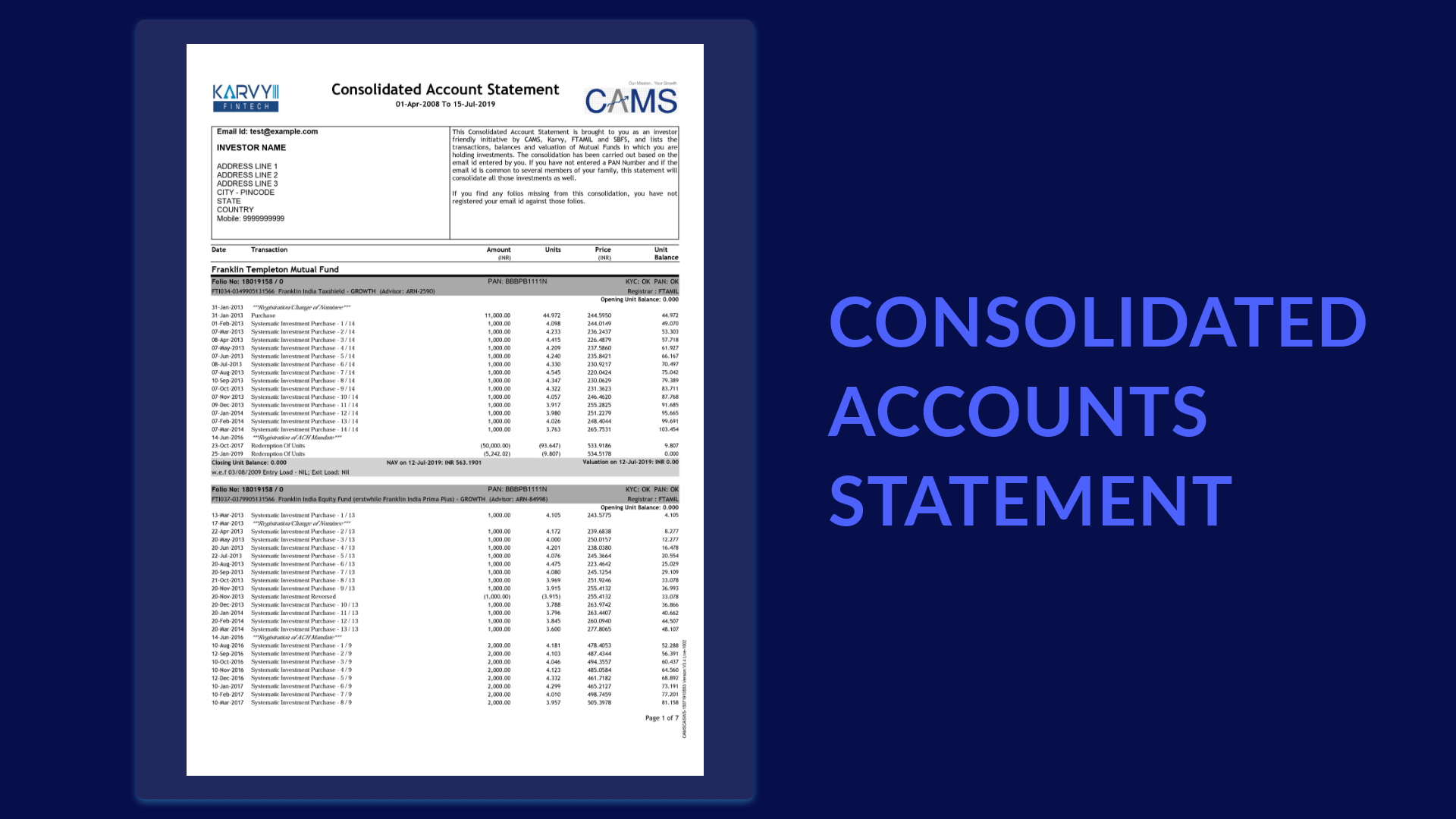

What is CAS? CAS, or Consolidated Account Statement, is an account summary that provides details of securities held in a demat account. Issued by depositories like NSDL and CDSL, CAS consolidates information from the Registrar and Transfer Agents (RTAs) and organizes it by PAN (Permanent Account Number), as provided by the Income Tax Department. CAS is made available both electronically and physically. The electronic version is sent to the email address registered with NSDL/CDSL, while the physical copy is mailed to the registered address. CAS includes details of all types of securities, including shares, bonds, mutual fund units, and government securities, held in a demat account across different brokers. If there is a transaction in the demat account, the statement is sent monthly. If there are no transactions, it is sent semi-annually.

What Has Changed? The capital market regulator has modified the CAS dispatch timeline. Mutual Fund RTAs send updated PAN-wise data to NSDL/CDSL, and the depositories process this data, dispatching the CAS to clients with a 7- to 10-day delay. Previously, AMCs had a deadline of the 3rd of the month for dispatch, and depositories had until the 10th. Now, the new timeline sets the AMC/MF-RTA deadline to the 5th, with depositories dispatching by the 12th. For clients who opt for electronic CAS, it will be delivered by the 12th of each month, while physical copies will be dispatched by the 15th. While the two-day extension may seem minor, it carries its own set of implications.

Lag in Data Dissemination: It is surprising that in an era of T+0 settlement and algorithmic trading, SEBI has allowed this extension in CAS dispatch timelines. The system involves around 50 AMCs, just 2 depositories, and approximately 300 RTAs (200 RTAs with CDSL and 100 with NSDL). With only about 350 participants in the system, a fintech solution could easily enable real-time updates of PAN-wise investment data among these stakeholders. With the number of mutual fund investors already at 22 crores and set to increase exponentially due to initiatives like the Rs. 250 JanNivesh SIP, further delays in the system could be problematic. If compliance deadlines continue to be extended, it could jeopardize the effectiveness of the entire system.

Repercussions of Delayed Dispatch: Many corporates and older investors rely on CAS to keep track of their mutual fund units and securities. A 12- to 15-day delay means they won’t have access to their portfolio details from the previous month until the middle of the current month—an unsatisfactory scenario. Investors may seek other options if they require consolidated portfolio statements sooner. SEBI must recognize these challenges and establish a framework for real-time CAS download to better serve investors.