In recent times, SEBI has issued numerous adjudication orders concerning cases related to illiquid stock options. The regulator has also been organizing settlement schemes to address these issues. In the 2024 settlement scheme, 768 entities settled their cases with SEBI. In this write-up, we will explore the concept of illiquid options, the rationale behind them, and how they have been used or misused by market participants.

What is an Illiquid Option Contract? Illiquid option contracts are those that suffer from low levels of trading activity, meaning there are few buyers and sellers. As a result, these contracts are difficult to trade, and the bid-ask spreads tend to be very wide. Discovering a fair price for such contracts is often challenging. Typically, illiquid options are deep in-the-money or deep out-of-the-money. For example, if the share price is Rs. 500, options with strike prices of Rs. 1000 or Rs. 250 would be illiquid.

The “Happy Ending” Game of Illiquid Options: Illiquid options facilitate a “happy ending” game, where two participants can enter a trade with the intention of transferring profits or losses between each other’s accounts. For instance, consider two traders: Gopal and Mahipal. Gopal has made a profit of Rs. 5 lakh during the year, while Mahipal has incurred a loss of Rs. 5 lakh. Gopal would normally have to pay tax at a rate of 30% on his Rs. 5 lakh profit. However, if he can somehow transfer this profit to Mahipal, Gopal can avoid paying tax, as Mahipal’s loss would offset the taxable amount.

To execute this scheme, Gopal and Mahipal choose shares of Reliance, which is trading at Rs. 1200. They agree on a strike price of Rs. 1600. Gopal sells a call option contract at Rs. 2, and Mahipal buys it at the same price. After a short while, Gopal buys back the option at Rs. 9, incurring a loss of Rs. 7 per unit, while Mahipal sells it at Rs. 9, making a profit of Rs. 7 per unit. This synchronized trade effectively transfers Rs. 5 lakh from Gopal’s account to Mahipal’s, neutralizing the tax implications. Since there is a 30% tax on derivative gains, Mahipal would return a portion of the profit to Gopal after deducting his commission (usually between 5% to 10%).

One might wonder why SEBI is concerned about such “magical” trades where both parties appear satisfied with the outcome.

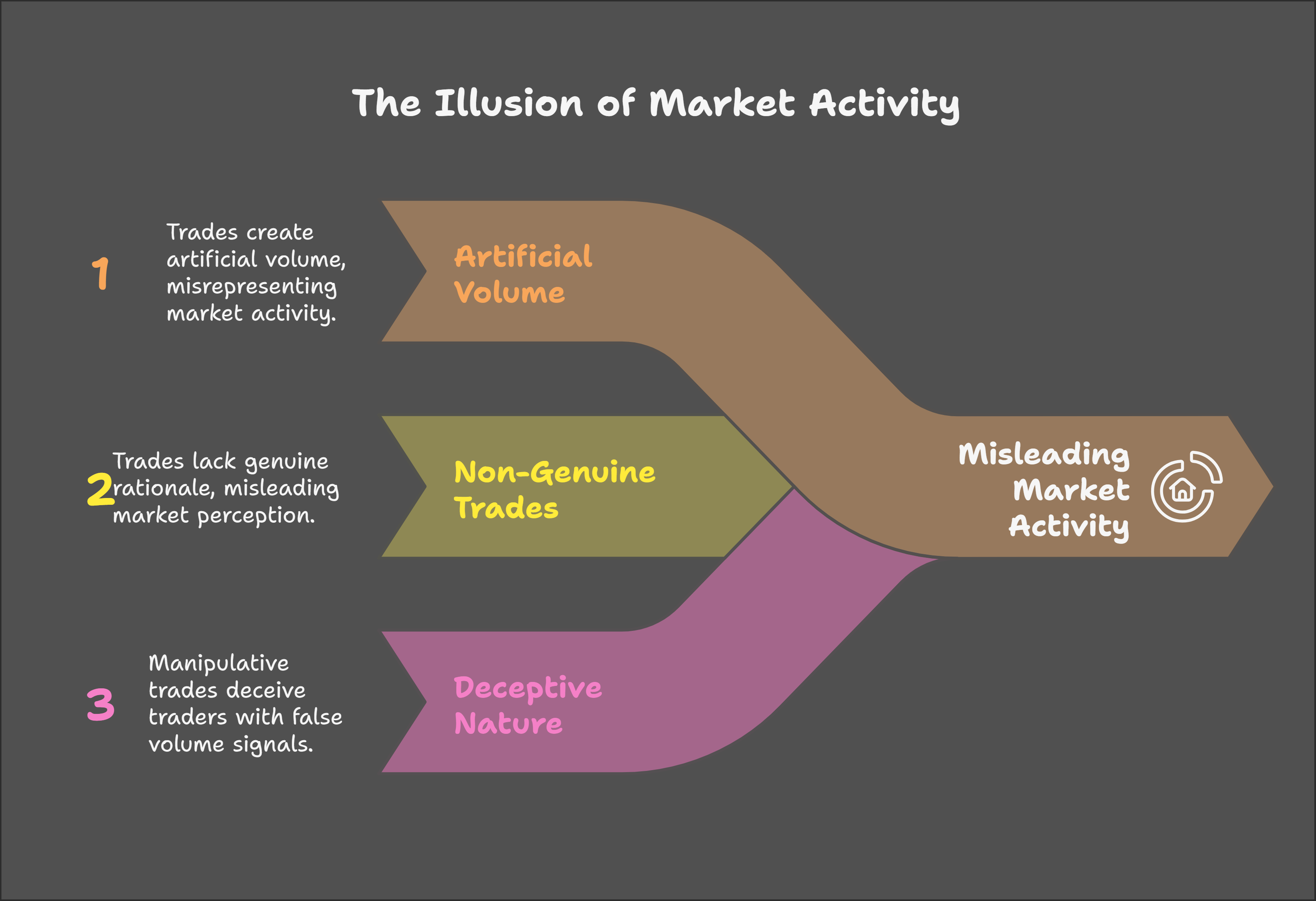

Why is SEBI Concerned?: SEBI has raised concerns about illiquid options trades, as they violate the SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003. In all its orders related to illiquid options, SEBI cites the creation of artificial volume and the manipulation of prices through reversal trades. The key points SEBI highlights are:

- Artificial Volume: Trades in illiquid options create artificial volume that does not reflect genuine market activity.

- Non-Genuine Trades: These trades lack the basic rationale for trading, as they are primarily designed to create a misleading appearance of market activity.

- Deceptive and Manipulative Nature: Such trades are seen as manipulative, as they can mislead other traders into entering the market based on false volume signals.

Importantly, SEBI is not concerned with the tax implications of these trades, as that falls under the jurisdiction of the Income Tax Department.

Why Does SEBI Allow These Trades? : It is perplexing as to why SEBI continues to allow illiquid options contracts, given their susceptibility to misuse. These options have long been prone to manipulation, and traders have consistently exploited them for tax avoidance and other unfair advantages. SEBI has caught numerous traders involved in such practices and imposed penalties on them. Additionally, SEBI has introduced settlement schemes to resolve these cases. It appears that SEBI and traders involved in illiquid options are, in a sense, working in tandem for mutual benefit. Traders gain by reducing their tax liabilities, while SEBI collects penalties, making it a win-win situation for both parties. In this scenario, the true loser seems to be the Income Tax Department.

What Should SEBI Do?: If SEBI is genuinely concerned about the misuse of illiquid options, it should take more decisive action. One option would be to discontinue illiquid option contracts, which are prone to manipulation. Alternatively, SEBI could enhance liquidity in these contracts by encouraging market makers to participate, which would make it more difficult for manipulative practices to thrive.